COT Report Formats Explained: Legacy, TFF, and Disaggregated

By The COT Data Team · Apr 9, 2026

COT Report Formats Explained: Legacy, TFF, and Disaggregated

When people say "the COT report," they usually mean one thing — but the CFTC actually publishes three different formats. Each one covers the same underlying positions but carves up the trader population differently. Using the wrong format for your market is not fatal, but it does mean you are looking at a blunter tool than you need.

This article explains what each format shows, how they differ, and which one is appropriate for FX, financial futures, and commodity markets. It does not constitute investment advice. All trading carries risk.

The Three Formats at a Glance

| Format | Best For | Trader Groups |

|---|---|---|

| Legacy | Physical commodities, broad overview | Commercials, Non-Commercials, Non-Reportable |

| TFF (Traders in Financial Futures) | FX, rates, equity index futures | Dealer/Intermediary, Asset Manager, Leveraged Money, Other Reportable, Non-Reportable |

| Disaggregated | Agricultural, energy, metals | Producer/Merchant, Swap Dealer, Managed Money, Other Reportable, Non-Reportable |

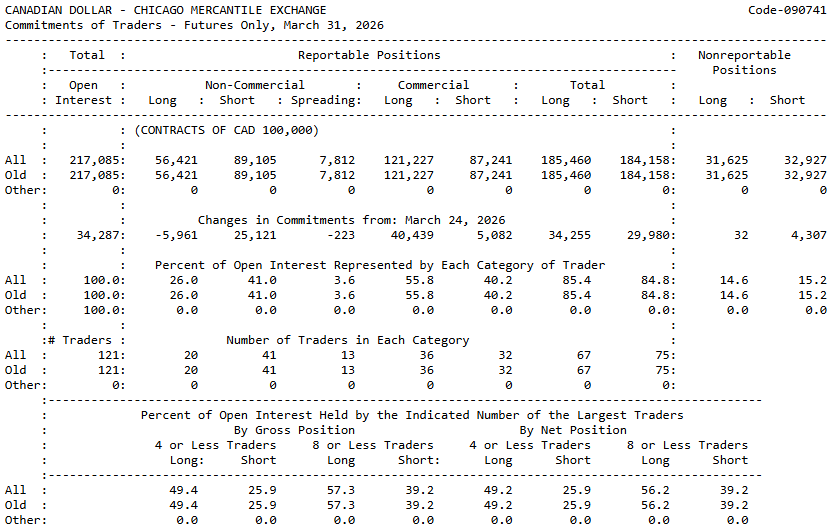

Legacy: The Original Format

Legacy is the oldest format and the one most commonly referenced in trading content. It divides all reportable positions into two camps:

- Commercials — entities that use the futures market to hedge a business exposure. A grain elevator short corn futures; an airline long crude oil. They are not trying to profit from the futures position itself.

- Non-Commercials — everyone else large enough to report. Hedge funds, CTAs, prop desks. These are speculative positions.

- Non-Reportable — the remainder after large traders are accounted for. Retail traders, small funds, miscellaneous participants. Also called Small Traders.

The appeal of Legacy is simplicity. The criticism is that it is a broad brush — it lumps a pension fund buying equity index futures as a hedge alongside a trend-following CTA betting on a breakout, and calls both "Non-Commercial."

For physical commodity markets — grains, energies, soft commodities — Legacy still works well. The hedger/speculator split is meaningful when one side actually produces or consumes the underlying.

For financial futures, it starts to blur.

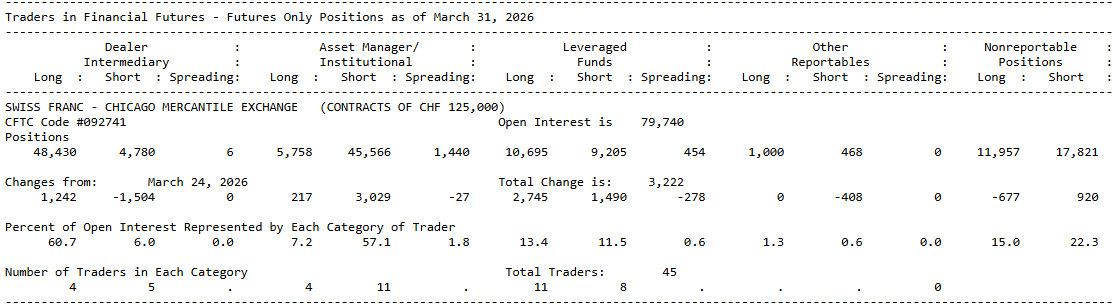

TFF: Built for Financial Markets

The Traders in Financial Futures report was introduced in 2010, specifically for futures with no physical delivery — FX, interest rates, equity indices, VIX. The CFTC recognised that the Commercial/Non-Commercial split was not very informative when nobody is hedging a warehouse of euros.

TFF breaks traders into four reportable categories:

- Dealer/Intermediary — banks and broker-dealers managing risk on behalf of clients. They are typically on the opposite side of institutional demand. If asset managers are buying EUR/USD futures, dealers are often the other side.

- Asset Manager/Institutional — pension funds, insurance companies, sovereign wealth funds. These are large, slow-moving positions driven by allocation mandates rather than short-term views.

- Leveraged Money — hedge funds and CTAs. This is the speculative signal. These participants are trading actively and their net position is the most watched figure in the TFF report.

- Other Reportable — entities that do not fit neatly into the above categories.

- Non-Reportable — same as Legacy: positions too small to require individual reporting.

If you trade forex — EUR/USD, GBP/USD, JPY futures — TFF is the appropriate format. The Leveraged Money group is your signal; it corresponds roughly to the Non-Commercial group in Legacy, but is cleaner because asset managers are separated out. A pension fund rebalancing does not mean the same thing as a CTA adding to a trend position, and TFF keeps them in different buckets.

Disaggregated: The Commodity Specialist

The Disaggregated report sits between Legacy and TFF in terms of adoption. It applies to physical commodity markets — grains, livestock, energy, metals — and splits the old Commercial category into two distinct groups:

- Producer/Merchant/Processor/User — entities with a direct physical relationship to the commodity. Farmers, miners, refiners, food processors. These are the genuine hedgers.

- Swap Dealer — financial intermediaries managing commodity exposure through swaps and other OTC instruments. A bank that has sold commodity-linked notes to retail investors will hedge that exposure in the futures market, showing up here. They look like hedgers in Legacy, but their motivation is financial, not physical.

The distinction matters because swap dealer activity can be large and directional, and in Legacy it is hidden inside the Commercial category — distorting what looks like hedger sentiment.

- Managed Money — same as Leveraged Money in TFF: CTAs and commodity hedge funds.

- Other Reportable and Non-Reportable — same as above.

The Disaggregated report gives the clearest picture for commodity markets, but it also requires more effort to read. Most retail traders stick with Legacy for grains and energy because the signal is good enough, and TFF for FX. That is a reasonable trade-off.

Which Format to Use

FX and financial futures (EUR/USD, JPY, S&P 500, 10-year notes): Use TFF. Focus on Leveraged Money net position. Dealer/Intermediary positioning can be used as a contrarian reference — dealers tend to be on the other side of institutional flow.

Agricultural commodities (corn, soybeans, wheat, cotton): Legacy or Disaggregated both work. Legacy is more widely available and easier to benchmark against historical data. If you want to isolate swap dealer noise from genuine producer hedging, use Disaggregated.

Energy and metals (crude oil, gold, silver): Same as agricultural — Legacy for a quick read, Disaggregated if you want the detail.

The COT dashboard on this site uses the Legacy format across all markets. It is the most portable format for a multi-market dashboard, and the signal quality for the markets covered is adequate. For FX specifically, the Non-Commercial group in Legacy and the Leveraged Money group in TFF tend to track each other closely — the same funds are driving both.

A Note on Timing

All three formats share the same reporting cycle. Positions are measured as of Tuesday close. The CFTC publishes the data on Friday, typically at 3:30 PM Eastern. That is a three-day lag. In a fast-moving week — a central bank surprise, a geopolitical event — the published positions may already be stale by the time you read them.

This is not a reason to ignore COT data. It is a reason to use it as a positioning context rather than a precise entry signal.

Limitations

- Legacy's Commercial group includes swap dealers. In commodity markets with heavy financialisation, this can overstate apparent hedger activity.

- TFF is only published for financial futures. There is no TFF equivalent for corn or crude oil.

- All formats report aggregate positions across all contract months. Rolling behaviour around expiry can cause distortions in the weekly change figures.

- "Non-Reportable" is a residual category, not a direct measure. It is total open interest minus what large traders report. Treat it as an indication, not a precise measurement.

Summary

Three formats, same underlying data, different lenses. Legacy is the workhorse — broad, widely used, good enough for most purposes. TFF is the right tool for financial futures and FX, where the hedger/speculator split is not meaningful. Disaggregated adds granularity for physical commodities by separating genuine producers from financial intermediaries.

Most traders only need to know two: Legacy for commodities, TFF for FX. The format you choose shapes which group you call "the smart money" — so it is worth getting right.

Current positioning across 41 futures markets is on the COT dashboard. No subscription required.

Data source: CFTC Commitment of Traders report, published weekly. This page is not affiliated with or endorsed by the CFTC. All data is provided for informational purposes. This is not investment advice.